Key Takeaways

- Always pause to verify. Check the lender against the official Registry of Moneylenders before sharing any personal information.

- Be aware. As of 2026, there are 153 licensed moneylenders in Singapore, according to updates from the Ministry of Law.

- Details should match exactly. A legitimate lender’s business name, licence number, office address, landline, and website must fully match the Registry record.

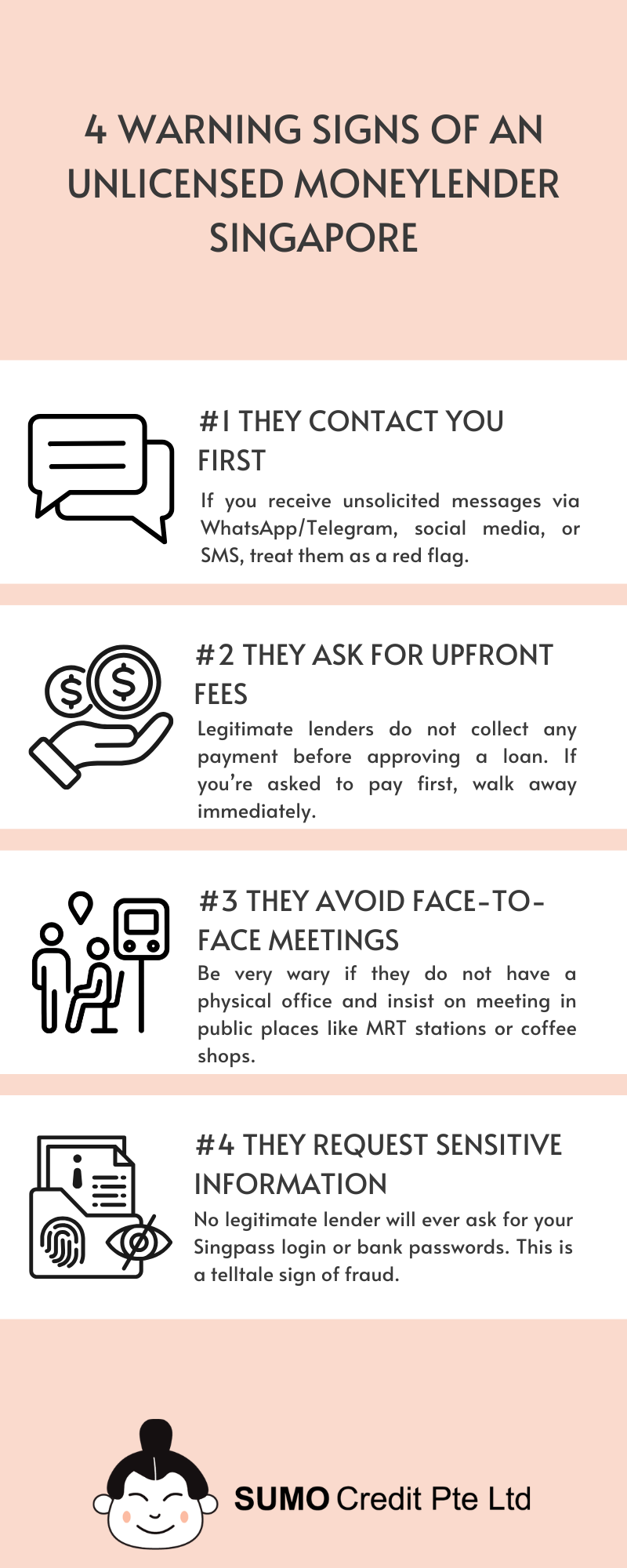

- Watch how they contact you. Licensed moneylenders are prohibited from soliciting loans via WhatsApp, SMS, phone calls, or social media ads.

- Trust your instincts. If something feels off, it’s best to walk away.

Taking a moment to verify a moneylender’s licence is critical. Loan scams in Singapore often begin with something seemingly innocuous—a friendly message, a tempting social media ad, or a website that looks completely legitimate. At first glance, everything may seem normal, and many borrowers only realise that something is off when it’s much too late.

It’s easy to verify a moneylender’s licence so long as you know what to look out for. Keep reading to find out how to check a moneylender’s licence status to ensure that you only deal with licensed moneylenders in Singapore and steer clear of unscrupulous loan sharks or ah longs.

What Is a Moneylender Licence in Singapore?

A moneylender licence is an official approval from the Ministry of Law that allows a company to legally offer loans in Singapore. Without it, any lending activity with interest is considered illegal.

As of 2026, there are 153 licensed moneylenders listed on the Registry of Moneylenders, and this number can change as licences are updated or revoked. Every lender on the list is assigned a unique moneylender licence number; for example, Sumo Credit’s licence number is 5/2026.

Being licensed means that lenders must comply with strict rules under the Moneylenders Act, including caps on interest rates and fees.

How to Check a Moneylender Licence in Singapore

Not sure if a lender is legit? Here’s a simple way to verify before you go any further.

Step 1: Start With the Official Registry of Moneylenders

Go straight to the official list of moneylenders on the Registry of Moneylenders website. Note that this is the only source you should trust—do not rely on screenshots, forwarded PDFs, or links sent via messages; these are often used by scammers to appear convincing.

Step 2: Locate the Lender’s Business Name

Search for the lender’s name and make sure everything lines up perfectly. Check for their:

- Licence number

- Registered business name

- Office address

- Landline number

Watch out for any discrepancies between the official source and the information provided by the lender. Even minor differences—such as a slightly altered name—can be a red flag.

Step 3: Check How They Reached You

How a lender contacts you matters more than you think; licensed lenders are only allowed to promote their services through:

✅ Their official website

✅ Approved business directories and consumer directories

✅ Their physical shopfront

They are NOT allowed to:

❌ Send unsolicited messages via WhatsApp/Telegram, SMS, or social media

❌ Make cold calls

❌ Run advertisements on social media

If a loan offer comes through a random message or ad, chances are, it’s part of a scam or illegal moneylending activity. Do not continue with the interaction; block the sender immediately!

Step 4: Verify the Physical Office

A licensed moneylender in Singapore must operate from its registered office. Before disbursing any loan, licensed lenders are required to:

- Conduct in-person verification of borrowers’ identities at their registered office premises

- Prepare clear, written contracts and explain them to the borrower in a language they understand

- Obtain the borrower’s signature on the contract

If the lender insists that everything should be done remotely or refuses to provide a written contract, alarm bells should start ringing. Stop engaging immediately.

Why Checking a Moneylender’s Licence Matters

Apart from the obvious reason of avoiding ah longs and unlicensed moneylenders, there is another lesser-known, but equally important reason why you should only borrow from licensed moneylenders in Singapore: you’re only backed by law when you borrow from a licensed lender. This means there are clear rules on how lenders operate and robust safeguards in place if things go wrong.

For example, if a lender engages in unfair practices such as excessive fees or harassment, you can report it to the Registry of Moneylenders or seek legal recourse through the Small Claims Tribunal or the Court. On the flip side, unlicensed moneylenders in Singapore are not subject to any regulations, which means you may very well be exposed to serious risks, such as harassment and extortion, with little to no legal recourse if you choose to engage with them.

How to Spot an Unlicensed Moneylender in Singapore

What to Do if You Encounter a Loan Shark in Singapore

If you suspect illegal moneylending or harassment, don’t ignore it. Save any evidence such as screenshots, messages, phone numbers, or payment requests. You can then lodge a police report or call 999 if you’re in immediate danger.

Bottom Line: Borrow Safely From a Licensed Moneylender in Singapore

Checking a moneylender’s licence is the most important step you should take before taking a loan in Singapore. A moment is all it takes to make sure you’re dealing with a legitimate lender registered with MinLaw.

If you’re looking for a legal moneylender in Singapore, Sumo Credit is a trusted licensed lender committed to transparent, responsible lending. Whether you’re looking for a personal loan, payday loan, instant loan, bad credit loan, or business loan, we have flexible options designed to meet your unique needs.

Ready to borrow with confidence? Apply now or reach out to us for a no-obligation chat on your options today.