Key Takeaways

- In Singapore, licensed moneylender interest rates are regulated. However, borrowers should still perform their due diligence and compare loan fees, loan tenures, and total repayment amounts before committing.

- For personal loans in Singapore, interest is charged only on the outstanding balance. This means that the interest payable reduces as the principal amount decreases.

- A lower advertised rate does not always mean a lower overall borrowing cost once tenure, fees, and repayment structure are taken into account.

- When comparing licensed moneylenders’ interest rates, it is safer to focus on transparency, contract terms, and whether the monthly instalments fit your budget.

- Always verify the moneylender’s authenticity through the official registry to ensure they are a legitimate business.

When taking out a loan, the most important consideration for borrowers is the interest rate.

The licensed moneylender’s interest rate is one of the first things borrowers compare when looking for loan options with good interest rates in Singapore. You must understand that even a small difference in the rate can affect how much you repay over time.

Still, the headline number should never be the only thing you compare. Other than interest rates, did you know there are other fees, such as admin fees and late repayment fees, that will be added to your loan? We’ll need to consider these as well.

Not to worry, this does not mean that borrowing from licensed moneylenders will inevitably drown you in debt. As mentioned, licensed moneylenders are regulated by the Ministry of Law, which sets maximum limits on the fees and interest that can be charged. Should the licensed moneylender fail to comply with these rules, their licences may be jeopardised.

This guide explains the basics in a practical way. It covers how licensed moneylender interest rates work, the legal safeguards that apply, how repayments are typically calculated, and what to look out for when comparing low-interest moneylenders in Singapore.

What Is a Good Licensed Moneylender’s Interest Rate in Singapore?

A good licensed moneylender’s interest rate sits anywhere from 1% to 4% a month; the lower the rate, the better.

A licensed moneylender’s interest rate is the amount the lender can charge for offering the loan. The percentage does not matter if the loan is secured or unsecured.

Furthermore, this interest rate must be stated clearly in your loan contract. If you are unsure of the terms and conditions in your loan contract, ask the loan officer to explain in a language that you are comfortable with before making a decision on whether to take out the loan or not. When taking a personal loan or a quick loan from a licensed moneylender, interest is calculated on the outstanding balance rather than the full original amount throughout the loan period. This is often referred to as the reducing balance method. In simple terms, as you repay the principal, the balance goes down, and interest will be charged on the lower remaining balance.

Why should you care? This matters because borrowers sometimes compare loans without understanding how the calculations work. A simple interest rate is, well, truly not so simple. A loan may look straightforward on the surface, but the repayment structure can make a significant difference to the total amount paid over the life of the loan.

What Are the Legal Interest Rate and Fee Limits for Moneylenders in Singapore?

Unlike loan sharks, who charge ridiculously high interest rates, licensed moneylenders in Singapore have legal caps to adhere to since 1 October 2015. These limits help to protect borrowers from unreasonable rates and fees.

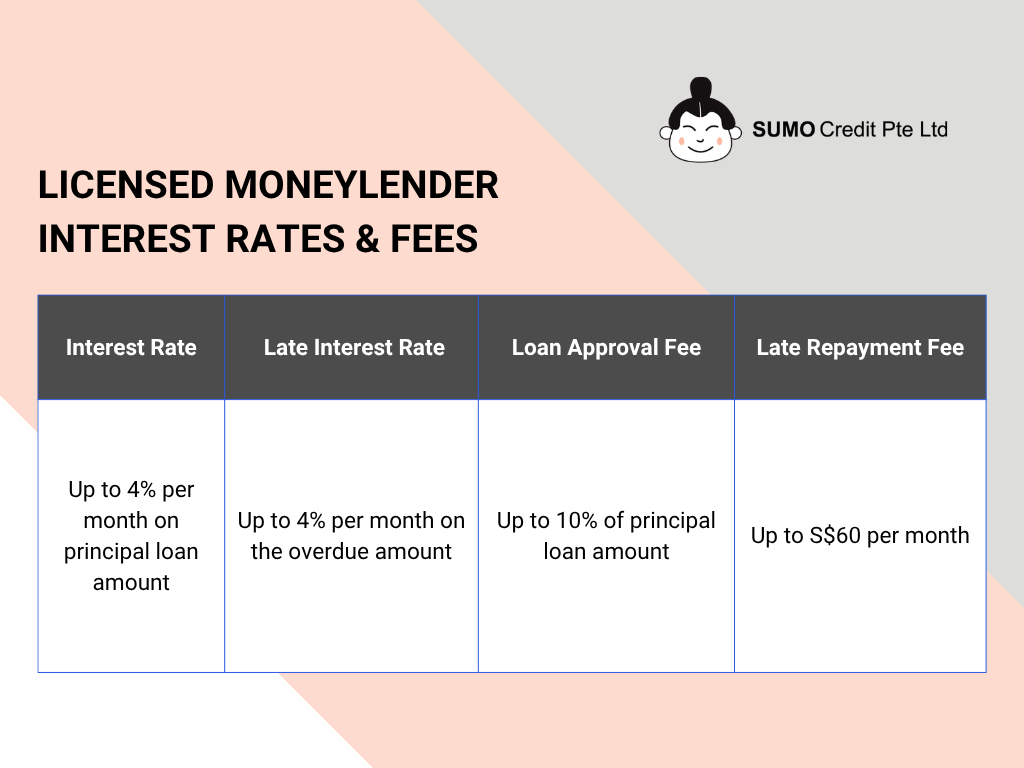

As illustrated above, the maximum interest a licensed moneylender can charge is 4% per month. There are no circumstances under which a higher interest rate can be charged, except in cases where business loans are concerned.

At the same time, the maximum late interest rate that can be charged is also 4% per month, applied only on the overdue loan repayment amount. This means the borrower is not exposed to open-ended charges if the lender is properly licensed and compliant.

Regarding fees, all legal moneylenders are not allowed to charge a fee exceeding 10% of the principal loan amount when the loan is approved. This is usually deducted upon loan approval. Lenders are also not allowed to charge a fee of more than $60 for every month of late repayment.

That’s not all. What many might not know is that the total sum—comprising interest, late interest, administrative charges, and all applicable late fees—cannot exceed the original principal loan amount!

Pro tip: Borrowers should not stop at checking the legal caps alone. A lender can still be within the law while offering a repayment structure that may not suit your financial situation. The better approach is to review the full contract and check the repayment schedule before committing to the loan contract. If you want to read the official framework, simply refer to the licensed moneylenders’ laws in your free time.

How Licensed Moneylender Interest Rates Are Calculated in Singapore

Licensed moneylenders calculate interest monthly based on the outstanding loan amount.

Here’s an example to help you understand the reducing balance method:

Mr Tan needed cash urgently and took out a $5,000 loan from a licensed moneylender. He was charged an interest rate of 3.9% per month for a 6-month loan tenure. Based on the reduced balance calculation, interest for the first month is calculated on the principal loan amount. Subsequently, the interest is then calculated on the lower remaining principal balance of $4,244.29. His monthly repayment will be an estimated amount of $950.71. This is provided that he makes timely repayment and no late interest rates and fees are charged.

This means the interest portion of each instalment should gradually reduce over time, even though the borrower is still making regular repayments with the same instalment amount. That is why two loans with the same principal amount can result in different total repayments, depending on the interest rate and the loan tenure.

It is also useful to separate interest charges from other costs. Interest is the cost of borrowing money. Administrative charges, late fees, and late interest are different from the standard licensed moneylender interest rate. Borrowers should avoid focusing only on the large-print rate and ignoring the fine print in the loan contract.

This is especially important when comparing private moneylenders’ interest rates. A rate that appears lower at first glance may not automatically lead to a lower total repayment if the tenure is longer or the repayment structure is less suitable.

Licensed Moneylenders Interest Rates vs. Bank Interest Rates

Borrowers often compare private moneylenders’ interest rates against bank loan rates, but the comparison is not so straightforward. Banks and licensed moneylenders charge interest rates differently, so a lower number in one place may not reflect the same type of calculation elsewhere.

In general, licensed moneylenders use the reducing-balance method for personal loans. That means interest is charged on the remaining principal. By contrast, banks use a flat rate calculation for loans.

Another point of confusion is the language people use online. Many borrowers use the phrase “private moneylenders’ interest rates” when they really mean licensed lenders outside the traditional banking system. In practice, the key question is not whether the lender is called private, but whether the lender is licensed and transparent about how their interest works.

Before comparing lenders, verify them through the official Registry of Moneylenders list.

What Affects the Interest Rate You Receive?

Not every borrower receives exactly the same loan plan. A licensed moneylender’s interest rate may be shaped by practical lending considerations.

The first factor that licensed moneylenders consider is whether you are able to repay the loan. A lender should assess whether the borrower can realistically manage the repayments based on income and existing financial commitments.

Next, they’ll consider the loan amount. Larger loans affect the repayment amount and may affect how the loan is structured.

The repayment period also matters. A shorter tenure may reduce the total interest paid, while a longer tenure typically incurs higher total interest charges.

Borrowers should also remember that lenders are expected to assess risk and suitability responsibly. That is why two borrowers asking for the same amount may still receive different repayment structures and different private moneylender interest rates.

How Do I Lower My Loan Interest Rates?

One practical way to reduce your overall borrowing cost is to shorten the loan tenure. A shorter repayment period can mean less interest paid in total.

Do not be afraid to discuss loan terms with your legal moneylender. Be honest about your situation and discuss with the loan officers to customise a loan plan just for you. Some borrowers focus only on approval and leave the repayment details for later, but this is where many cost misunderstandings begin.

Improving your financial profile can also help in the longer term. Manage existing debt well, make timely repayments, and avoid unnecessary borrowing.

Where appropriate, some borrowers may also consider refinancing or structured debt solutions, but this should only be done after carefully comparing the full cost rather than reacting to a single advertised rate.

How to Compare Low-Interest Moneylenders and What to Check Before Accepting a Loan?

When borrowers search for low interest moneylenders, they are usually hoping to find the cheapest option. But in practice, the safest comparison is not based on the headline rate alone. It should include the full borrowing cost, the repayment terms, and the lender’s transparency.

- Check against the Ministry of Law’s list of licensed moneylenders to see if the lender is legal.

- Look at the loan contract and repayment schedule offered.

- Ask for calculations and explanations, find out the upfront fees you need to pay, the monthly repayment and the overall cost.

- Find out what happens if you were to repay late.

For loans, a Singapore moneylender’s interest rate should always be considered together with the repayment period and all applicable fees. For example, a loan with a slightly lower rate but a longer tenure may still cost more overall than a loan with a slightly higher rate and a shorter, more manageable repayment period.

You should also pay attention to how clearly the lender explains the contract. A lender that is transparent about the numbers, payment dates, and borrower obligations often gives borrowers a better basis for decision-making than one that relies on vague advertising.

You can also review your borrower rights before proceeding. That can help you understand which protections apply and what a good licensed moneylender is expected to disclose.

Why Borrowers Choose Licensed Moneylenders Like Sumo Credit

Before applying with any licensed moneylenders, the smart move is to check their public reviews and research their reputation.

Are they well-received by the other borrowers? Are there many complaints made against the lender? How about compliments? Is the feedback positive? These are honest, key indicators of whether the licensed moneylender you are looking at is good and suitable for you.

That is also why borrowers choose licensed moneylenders like Sumo Credit. The decision is often based not only on the interest rate offered, but also on whether the lender communicates clearly, explains the contract properly and patiently, and provides a repayment structure the borrower can fully understand. This matters even more when borrowers want to find a low-interest moneylender.

If you want to learn more about our borrowing process or ask questions directly, you can contact us anytime you are ready. Feel free to ask any questions; our friendly staff will be here to assist you.

You may also read Sumo Credit reviews to find out why our customers love working with Sumo Credit! Once you are convinced we are the trusted lender of your choice, you may apply online conveniently!